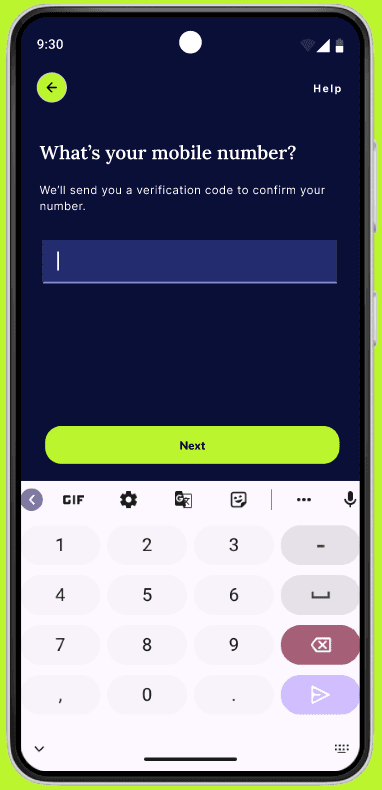

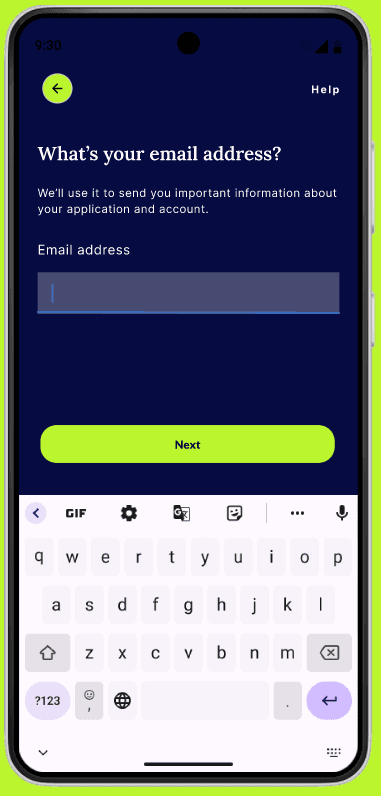

"I strategically increased the size of frequently used buttons and placed them closer to the users’ initial

touch points. For instance, I enlarged the primary call-to-action buttons and positioned them within

easy reach to minimize the movement distance required."

"Fitt's law states that the time required to move to a target area is a function of the distance to the target

and the size of the target."

Users are introduced to common financial terminologies and their brief definitions on the splash

screens itself.

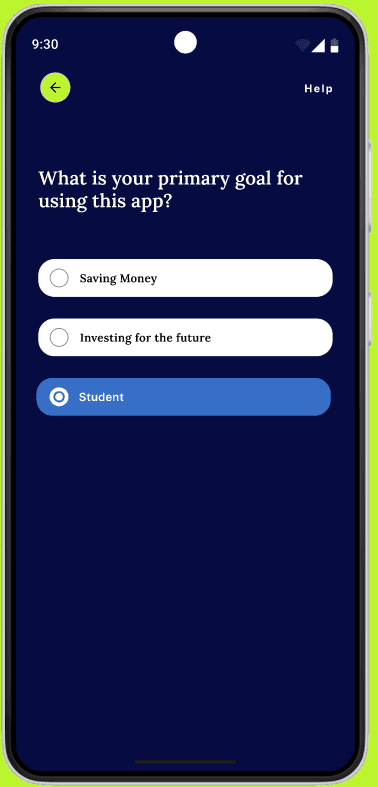

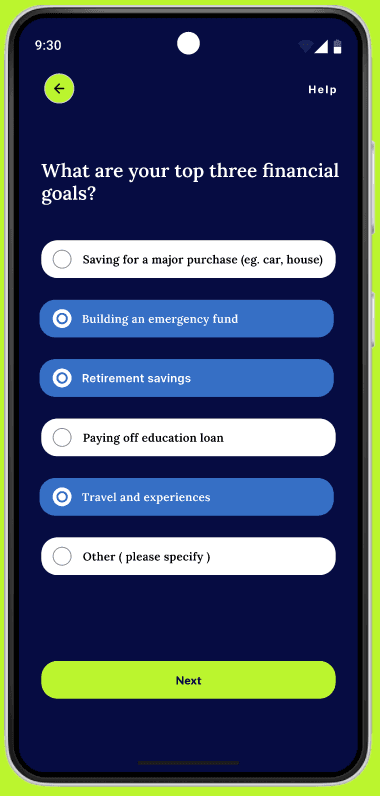

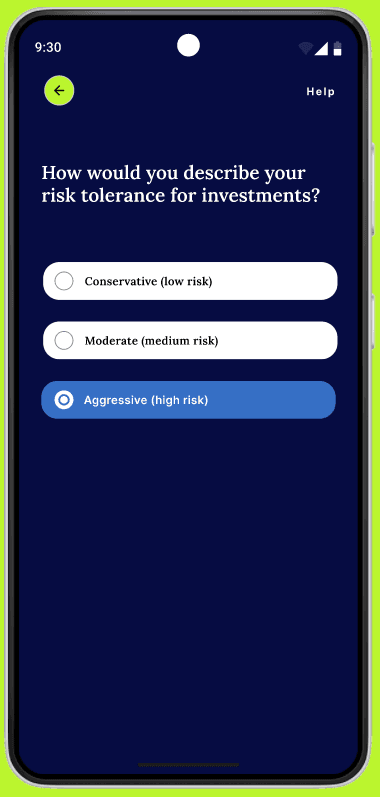

Users can completely personalize their savings and investment experience by answering a few

questions during onboarding and can manage these preferences later from their account settings.

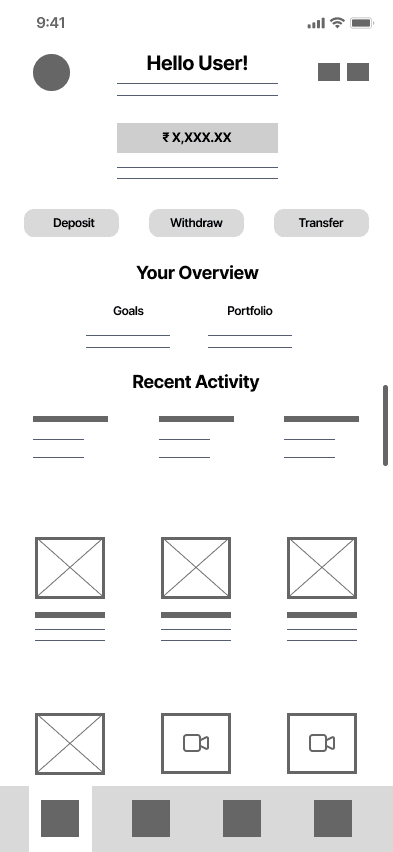

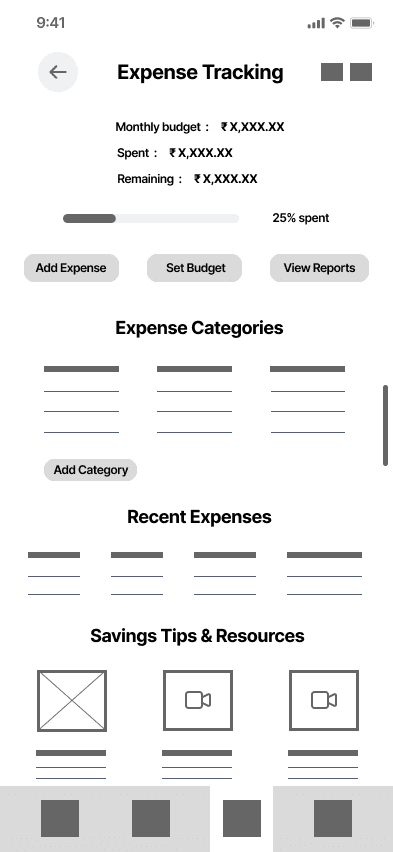

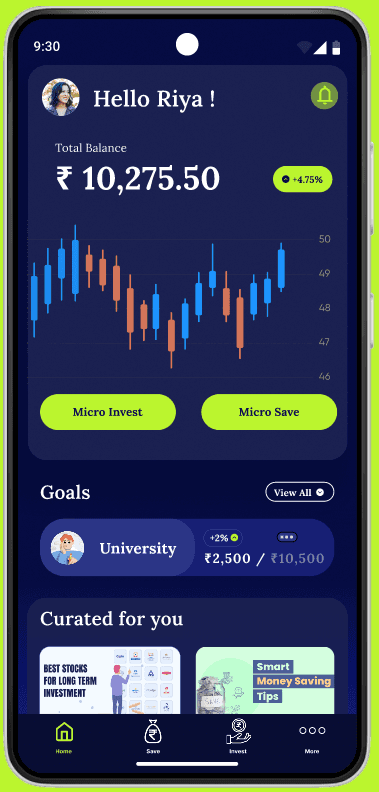

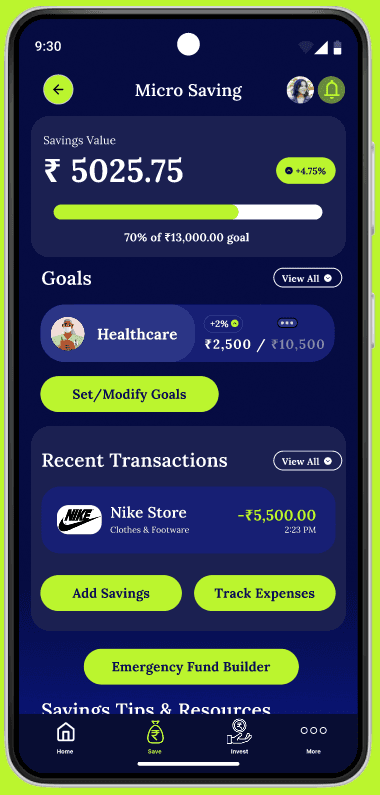

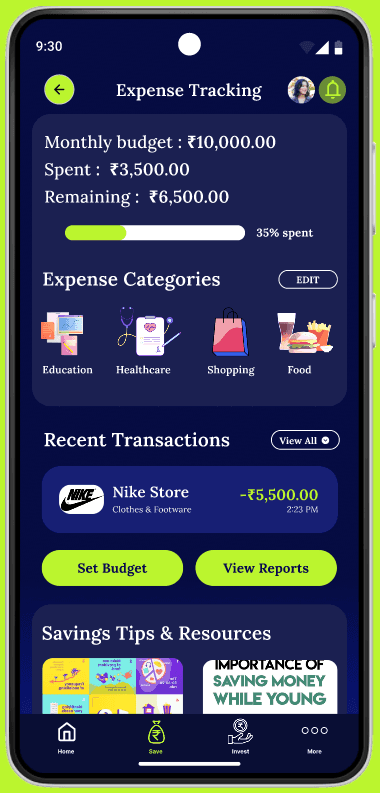

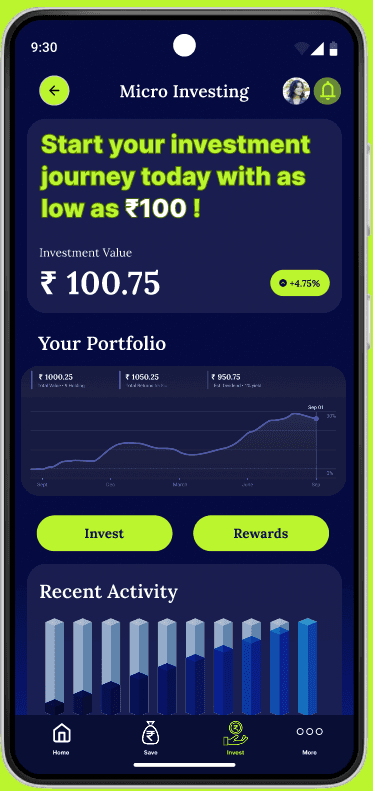

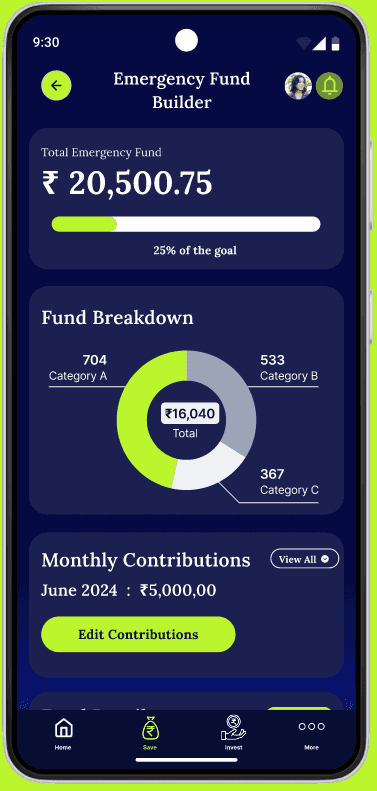

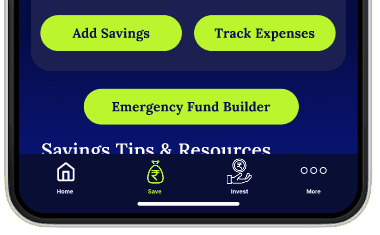

Users have dedicated sections for managing their expense, micro investing, micro saving and

building emergency funds.

Crafting Characters: The Journey of Customer Profiles

From this research, I developed two distinct user personas Veronica and Rohan that encapsulate the diverse needs and goals of our

audience. Veronica wants to try her hands on micro investing for the first time and Rohan is a man with responsibilities looking for a

simple and time saving user experience.

With my information architecture solidified, I turned my attention to craft the journey itself : the user flows. Like choreographers

orchestrating a ballet, I aimed to choreograph seamless interactions that would lead users from entry to fulfillment.

Energized by the wealth of ideas generated during the Crazy 8s session, I set out to shape these concepts into a coherent

structure: the information architecture. I began to organize my ideas into logical flows and pathways.

Under profile section, users will further be able to manage personalization in an elaborated way.

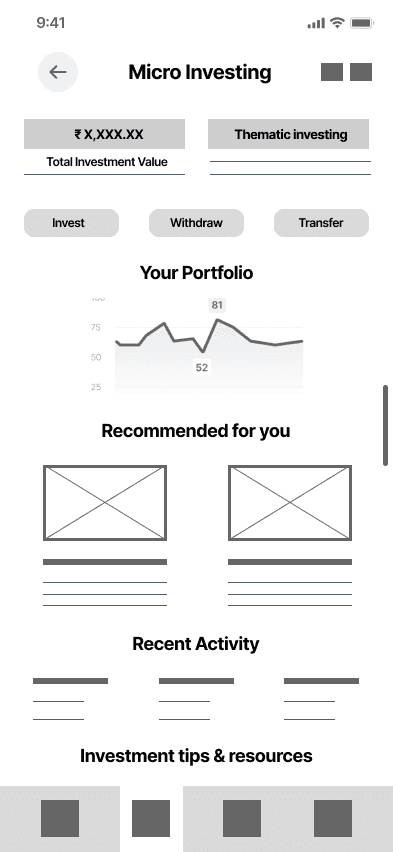

Under micro investing section, users will be able to view options like investment options, portfolios, performance tracking,

overview and features like thematic investing.

Under education and resources section, users will be able to see sub sections like articles, workshops, podcasts, finance

dictionary and other important tools like retirement, interest calculator, budget planner etc.

User Journey Safari

SOLUTION

WealthWeave is an app specifically designed for Gen Z and Millennials, allowing users to fully personalize their savings and investment

experiences. It provides tailored tools and insights based on individual preferences. Additionally, WealthWeave features a dedicated

section for tracking and managing expenses, a knowledge hub for financial terminology, and an emergency fund builder.

User wants to set up and use

emergency fund builder

User wants to track and manage

their expenses

Project Type

April 2024 - June 2024

( 12 weeks)

Micro Investment and

savings app concept

My Role

Product Designer

Project Timeline

Project Stack

Figjam, Figma, Notion

Framer

PROBLEM

Millennials and Gen Z face challenges in developing enduring savings

and investment habits

Although financial literacy and investment interest are growing among millennials and Gen Z, many face challenges in developing

enduring savings and investment habits due to perceived barriers and a lack of accessible, tailored tools. Trying to address this gap

to help them build sustainable financial practices and secure their financial future.

The Journey Begins: Discovering User Needs

RESEARCH

Carrying out survey

After surveying 23 individuals and analyzing their responses, I found several primary reasons (pain points) why users struggle to

establish sustainable savings and investment habits which defined my user goals :

Inefficient maneuverability/lack of custom options

complex jargon

insufficiency in informative material regarding investment and risk elements

absence of reward features

Before delving into design elements, I aim to investigate the psychological factors and motivations that drive goal setting. So, I

developed a survey to identify the issues users encounter while developing savings and investment practises.

65% of contributors frequently deal with obstacles like behavioral problems,

lack of knowledge, fiscal limitations, apprehension of hazards, and a lack of

motivation or rewards.

60% of people feel that there's a need for an uncomplicated and fun

micro-investment and savings tool, since they're open to sharing their

personal finance data, encompassing income and regular/periodic costs.

Key insights from survey responses

Take the survey on Google form

View survey results in Google sheets

Interacting with the users through interviews

Do you have any concerns or reservations about micro-investing that you would like

addressed?

Can you describe a scenario where having a robust savings and investment strategy

would significantly impact your life positively?

Can you walk me through your typical process for categorizing and monitoring your

expenses?

How would you like to balance risk and reward in your investment portfolio? Are you

more risk-averse or willing to take on higher risks for potentially higher returns?

Let's group similar notes together

I then organized my survey and interview data to gained some valuable insights that would surely help toshape my design decisions.

There were three themes which I could figure out namely : Challenges, Needs, User interface decisions

Time for the clash of titans : Analyzing our competitors

With an abundance of micro-investment applications accessible in the market, I executed a comparative analysis to comprehend

their distinct selling points (USPs), functionalities, benefits, and drawbacks. Below are some crucial points of interest.

Features

No social and community features

USP

Acorns USP lies in its automated investing

and savings features

Advantages

Diversified Portfolios

Recurring Investments

Found Money Program

Disadvantages

Fees for Small Accounts

Limited Investment Control

Lack of In-Depth Analysis Tools

Customer Service Limitations

Features

No tax efficiency features

USP

It simplifies savings by automatically

analyzing spending habits and effortlessly

transfers small, manageable amounts into a

secure savings account.

Advantages

Automated savings

Goal tracking

Overdraft protection

Disadvantages

Subscription fee

Limited Investment Control

Potential over-saving

Features

No account insurance feature

No social and community features

No gamification

USP

Betterment's USP is its goal-based investing and automated portfolio management, which uses advanced algorithms to optimize returns and minimize taxes for users of all experience

levels.

Advantages

Automated Portfolio Management

Goal-Based Investing

Tax Efficiency

Disadvantages

Management Fees

Limited Investment Choices

No Direct Stock Trading

Account Minimums for Premium Services

Features

No auto investing feature

No portfolio management tools

No risk assessment and guidance

USP

Qapital's USP is its unique approach to savings

automation through customizable rules and goal-

based savings, helping users effortlessly save

towards specific financial objectives.

Advantages

Customizable Savings Rules

Goal-Based Savings

Automated Savings Transfers

Integration with Banks and Services

Disadvantages

Subscription Fees

Limited Investment Options

Complexity for Some Users

Potential Banking Integration Issues

DEFINE

Concluding the empatize/research phase !!

In conclusion, the empathize phase of my project aimed to deeply understand the needs and behaviors of our users.

With a hand full of insights about user needs, pain points, choices and much more I move forward to the define phase.

Veronica / 18 / Student

Veronica, a second-year B.Tech student, relocated to Delhi a year ago

to pursue her engineering degree. Hailing from a middle-class family,

her parents secured an education loan for her studies since they both are

salaried employees. Veronica receives a modest allowance from her family

to manage her monthly expenses. With aspirations to begin micro-saving

and investing, she seeks to cultivate financial independence despite her

limited resources.

Frustrations / Pain Points

Poor expense management.

Limited understanding of financial terminology.

Limited access to financial planning resources.

Fear of risks while investing.

Shortage of incentives.

No rewards in return.

Confusing user interface.

Poor navigation/accessibility within apps

Rohan / 28 / Working Professional

Rahul, a marketing professional residing in Mumbai, is married, and both

he and his wife work, both remain very engaged with their work. He

occasionally faces challenges in managing multiple tasks simultaneously.

Additionally, he is considering family planning and aims to establish funds

for his future child. He frequently engages in reading about stocks and

financial matters and keep looking out for simpler resources available out

there.

Frustrations / Pain Points

Because of his busy schedule, he doesn't have sufficient time to

efficiently monitor his household expenses.

Limited investment growth opportunities.

Taxes applied on various platforms.

Security of his and his family's personal information.

Existing apps lacking personalized features.

With my personas vividly painted I embarked on the next chapter of our journey: crafting their digital adventures through customer

journey maps. As I started mapping these journeys, patterns and opportunities emerged. I identified key moments of truth—critical

touchpoints where user satisfaction could soar or stumble. Each map was a tapestry of insights, illustrating where my design

interventions could make a meaningful impact on user experience.

Let's start with Rohan's journey

Now, let's have a look at Veronica's journey

Empathy Map for Veronica

OUTCOME

After gathering all the touch points and pain points I conducted a 5 why analysis for each of my user's pain points to unravel the

mystery until I managed to reach the core issue. Each why brought me closer to the root cause.

Root cause explorer - finding the "5 Whys" ?

For Veronica's pain points

For Rohan's pain points

After uncovering the root cause of user frustration through my 5 Whys investigation, I framed several how might we statements to

turn my research findings into actionable design challenges which helped me taking my process forward.

Framing the HMW statements

HOW MIGHT WE

Moving to ideation

In the define phase I crystallized key user insights and pain points which helped me in providing a clear focus for my

design efforts. This phase helped me in synthesizing research data into some actionable problem statements and

set the foundation for ideation. Defining my user goals to be simplifying the process of expense tracking and coming

up with some convinient and time efficient solutions for busy individuals so that they can start to prioritize and manage

their finances.

So, taking my HMW statements as invitations to innovate. I did the crazy 8 session with 4 more people to get the splash of diverse

and inventive ideas - some practical, some imaginative, all valuable. These Crazy 8s sketches laid the groundwork for the next

phase of my design journey, turning my HMW statements into tangible design possibilities

Crazy 8's - 480 seconds of pure creative explosion

simplify the process of tracking expenses and clearly

communicate its benefits to overcome the belief that it

is time-consuming or complicated?

create convenient and time-efficient solutions for busy

individuals to prioritize and manage their savings

and investments?

Information Architecture

Defining user flows

User wants to register themselves

and start onboarding

User wants to access

financial education

resources

User wants to access and set

personalized savings goals

User wants to access and

practise personalized

micro investing

I also interviewed 5 people : 3 college students, 2 working professionals

"Ease of use is paramount. And it should be secure and trustworthy. Flexibility is also

important. I'd prefer a platform that allows me to invest small amounts regularly,

giving me the freedom to start with minimal funds and gradually increase my investment

over time as I become more comfortable with the process."

"An intuitive user interface and seamless navigation is key for me. And goal tracking

functionality would be essential. Being able to set and track progress towards financial

goals sounds attractive. And a feature that analyzes my risk tolerance, financial objectives,

and current portfolio to provide tailored investment suggestions would save me time and

potentially improve the performance of my investments."

"An intuitive user interface and seamless navigation is key for me. And goal tracking

functionality would be essential. Being able to set and track progress towards financial

goals sounds attractive. And a feature that analyzes my risk tolerance, financial objectives,

and current portfolio to provide tailored investment suggestions would save me time and

potentially improve the performance of my investments."

Some responses to look at

Empathy Map for Rohan

Some key takeaways from the empathy maps and personas

Veronica wants to begin with savings and investment practises but hesitates due to their complex interfaces, also

currently she tries to monitor her expenses manually but struggles with consistency.

Rohan wants to efficiently manage and monitor his household expenses but fails to do so beacuse of his busy

schedule, he also aims to estabilish a financially strong future for his family with minimal effort.

High fidelity wireframes

With my paper wireframes serving as the foundational blueprint, I embark to bring my vision into life by combining the best of the

explorations to form high fidelity wireframes. I immersed myself into refining details, I tried to craft each click and interaction very

carefully, tried to transform my concepts into tangible design elements.

High fidelity wireframes

Low fidelity wireframes

With my user flows meticulously plotted, I transitioned to the next phase of our design journey: crafting the blueprint for my interface

through low-fidelity wireframes. Armed with markers and sketch pads, I embarked on translating my user flows into visual

structures. Each wireframe was a rough draft, a skeleton outlining the placement of elements and functionalities without the

distraction of visual details. From login screens to product pages, I mapped out the flow of information and interactions,

prioritizing clarity and usability.

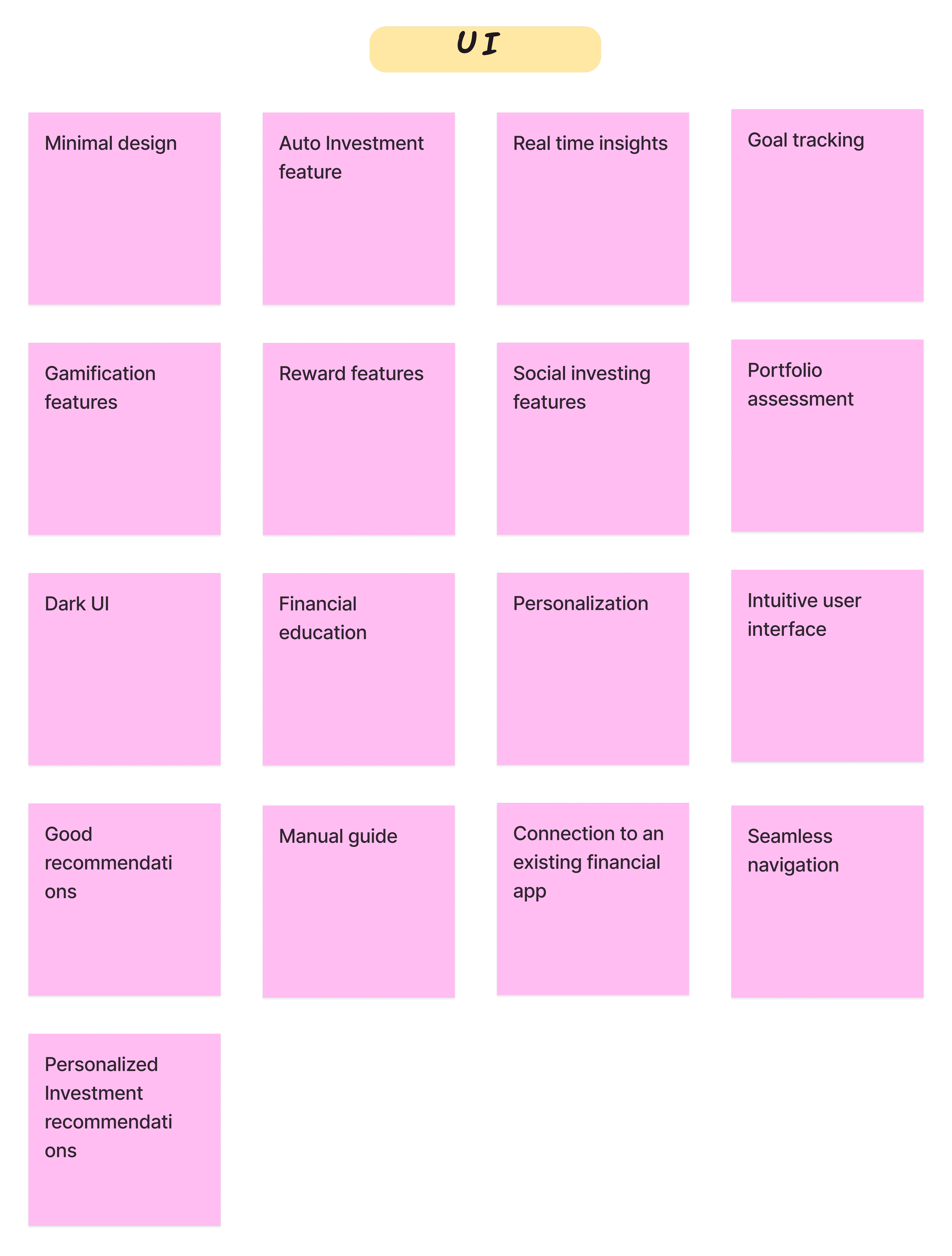

My top 3 takeaways from Crazy 8

Personalized onboarding setup for users which they can also edit and manage later on according to thei preferences.

A dedicated section to emergency fund builder.

Including features like : debt tracker, interest and retirement calculator, financial educational resources

Visual design elements

IDEATE

Icons & Typography

Ag

Lora

Ag

Lora

Logo

0D113F

17258A

18489F

BBF52E

18489F

Colors

Flow for accessing home screen, micro investing and savings screen, expense tracking screen and emergency fund builder followed by some explorations of the same flow.

Final Solutions / Outcomes

Inclusion of Fitt's law

Designs that were trashed !

I came up with few designs initially but ended up trashing them as they were not very aesthetically pleasing to me, also I came across

some readability issues with these designs. Let me know what you all think about these as well.

Conclusion

What did I learn?

Working on a complete project of app development was tough but a fruitful journey.

Got my hands on conducting user surveys and interviews to gather valuable insights.

Learnt to be flexible and adaptable to changes and new information throughout the project.

Finally, I would say that making a product both aesthetically pleasing and at the same time user friendly is difficult.

What were the challenges that I faced?

Experienced self-doubt and questioning my abilities and decisions throughout the project.

Ensuring visual and functional consistency across different parts of the project, especially when working on different aspects

simultaneously.

What I could have done better?

Initially I also thought of exploring and adding an augmented reality feature in my product but was not able to complete the

research eventually so, I had to drop that idea but in the next iteration I will try to add this up and would love to see how it is going

to impact

I would also work on improving my visuals further and do more iterations based on user feedback.

I will take a leave on Benjamin Franklin's quote, “Tell me and I forget. Teach me and I remember.

Involve me and I learn.”

For any feedback, suggestions or collaborations reach out on Linkedin